Understand EU Policies and Regulations

Environmental Defense Fund

The European Union (EU) has implemented various policies that address climate change, reduce greenhouse gas emissions, and promote the transition to a low-carbon economy. Companies that are involved in the EU market should stay informed about these policies and regulations and take steps to manage their climate-related risks and opportunities.

The EU has been at the forefront of global efforts to address climate change with a range of policies and regulations aimed at reducing greenhouse gas emissions. As a result, companies that do business in the EU market may be impacted by these regulations. In particular, companies need to understand the Corporate Sustainability Reporting Directive (CSRD) and the supporting European Sustainability Reporting Standards (ESRS), as well as the EU Corporate Sustainability Due Diligence Directive (CSDDD). CSRD will require companies to disclose how sustainability risks and opportunities affect their financial performance, as well as the impact of company’s operations on people and the environment. CSDDD introduces a legal obligation for large companies to identify, prevent and mitigate adverse human rights and environmental impacts in their operations and value chains. As part of the EU’s suite of sustainability regulations that push for transparent, responsible supply chains is the EU Deforestation Regulation (EUDR) which requires companies to ensure that the products they sell or export to the EU do not come from land that was recently deforested or degraded.

Additionally, companies should be aware of the European Union Emissions Trading System (EU ETS) -which is a cap-and-trade system aimed at reducing emissions from power and heat generation, industry, aviation, and maritime transport–, and the Carbon Border Adjustment Mechanism (CBAM) which applies duties to the import of certain energy-intensive products. Companies operating in the EU, including non-EU companies, may be subject to emissions allowances or other requirements under this system.

Even if your business is not covered by the new reporting requirements, you may still feel the impact of these changes, as supply chain emissions will be part of the scope of affected companies, so suppliers of EU companies may receive ESG questionnaires to provide data to their clients. Therefore, it is crucial for companies with significant EU operations to prepare for regulatory requirements by evaluating how they will be affected and educating their team internally to be prepared for upcoming changes.

Corporate Sustainability Reporting Directive (CSRD)

The EU’s CSRD will require in-scope companies to disclose the full range of sustainability matters (Environment, Social and Governance) using a double materiality lens, meaning you must disclose both how sustainability issues affect your business financially and how your business impacts people and the environment.

The 2025 omnibus I simplification package has narrowed the scope and delayed later phases. The omnibus I was officially adopted on Feb 24th:

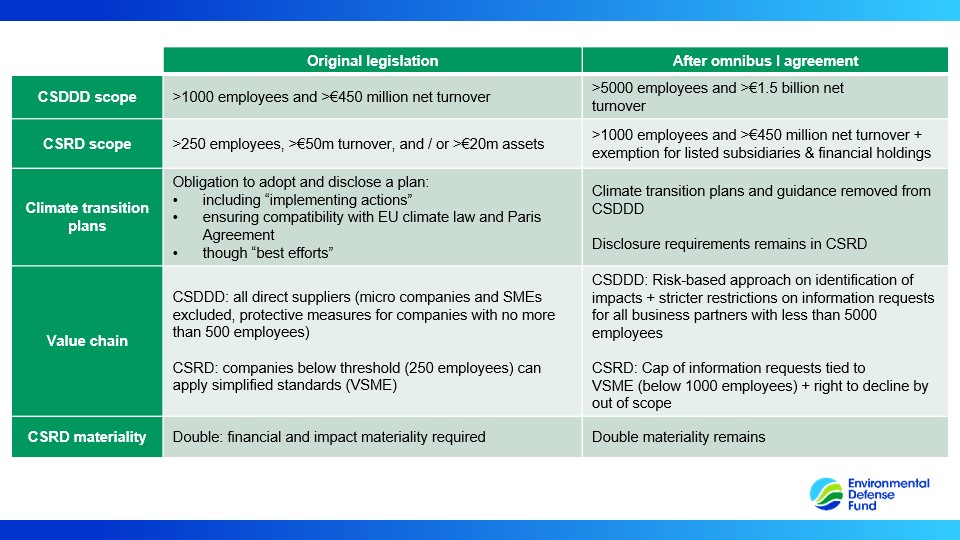

- Only very large companies remain in scope. Only EU-based companies with ≥ 1,000 employees and >€450 million turnover must report going forward (subject to a review clause). A threshold of over €450 million in net turnover is also proposed for non-EU based entities, and having a subsidiary or a branch in the EU exceeding € 200 million net turnover with no employee threshold.

- Listed Small and Medium-sized Enterprises (SMEs) are fully exempt, marking a substantial shift from the original framework.

- Value chain cap: safeguards have been introduced for companies in the value chain – companies that fall below the threshold of 1,000 employees; the information requests are limited to the information included in the voluntary sustainability reporting standard.

- Permitted information omission: companies may omit certain information, such as commercially sensitive, classified or IP-related information if certain conditions are met.

- Sustainability assurance: limited assurance remains mandatory with a limited assurance standard to be adopted no later than 1 July 2027

- The initial wave starts with reports covering FY 2027 (reporting in 2028) for EU-based companies, and FY 2028 (reporting in 2029) for non-EU based entities. Entities that are already reporting under CSRD before the omnibus will need to continue reporting unless relevant Member State opts to exempt them.

Practical steps for your company to prepare for compliance:

- Assess if and when your company falls in scope and identify the initial reporting year.

- Treat this as an enterprise-wide change: educate your executive team and relevant departments, such as finance, sustainability, legal, IT operations. Build a cross-functional working group to steer the reporting preparations.

- Compare your current ESG reporting to CSRD/ESRS requirements to identify gaps in data, systems and processes. Please note that the ESRS are currently undergoing a simplification process, with revised standards expected to be finalized during summer 2026.

- Start data collection early. Be ready to collect and disclose quantitative and qualitative data on a wide range of topics (from greenhouse gas emissions and energy use to workforce diversity, human rights due diligence, and anti-corruption measures).

- Begin conducting double materiality analyses as part of your annual risk assessment and strategy planning. This will not only prepare you for reporting but also help uncover business risks and strategic opportunities

- Engage with industry groups for the latest guidance and be ready to adapt your plans.

- Even if your company itself won’t report until later or is exempt, be prepared to respond to data request from your customers or partners as part of their CSRD compliance.

European Sustainability Reporting Standards (ESRS)

The ESRS are the detailed reporting rules under CSRD. The first set of ESRS came into effect in January 2024 but they are currently being revised as a consequence of the changes introduced in CSRS with omnibus I. It is a mandatory system of sustainability standards that applies to companies that fall within the scope of CSRD. Companies that are required to report under ESRS will be, to a great extent, ready to report under the International Sustainability Standards Board (ISSB) standards on climate-related disclosures, excluding few exceptions introduced as part of the revised ESRS.

The European Financial Reporting Advisory Group (EFRAG) introduced the ESRS Knowledge Hub as a central resource for businesses. This hub provides official documents, implementation guidance, educational materials, and interpretations to support organizations in meeting ESRS requirements.

The European Union initially intended to implement mandatory sector-specific standards for industries such as banking, agriculture, and oil and gas. This approach is now being eliminated as part of omnibus I. The European Commission may instead opt for non-binding, sector-specific guidance designed to help firms apply existing standards, rather than establishing new mandatory disclosure requirements for each sector.

Corporate Sustainability Due Diligence Directive (CSDDD)

The EU’s CSDDD introduces mandatory human rights and environmental due diligence obligations for large companies operating in the EU. It aims to ensure that businesses identify, prevent and mitigate adverse human rights and environmental impacts across their operations and value chains. CSDDD requires companies to conduct due diligence to identify and address those impacts and integrate due diligence into corporate policies and risk management systems. It also requires companies to establish grievance mechanisms for affected stakeholders and monitor and publicly communicate on due diligence efforts.

Under the revised scope agreed in the 2025 Omnibus package, CSDDD will apply to:

- EU companies with more than 5,000 employees and €1.5 billion in global net turnover

- Non-EU companies with equivalent thresholds for EU turnover

First time application is delayed to 2029.

Table: Final omnibus I agreement vs. original.

Practical steps for your company to prepare for compliance:

- Determine whether your company falls under the revised thresholds for applicability

- Map high-risk areas in your operations and supply chain

- Review and update existing due diligence policies and procedures to align with CSDDD expectations

- Establish or enhance grievance mechanisms and stakeholder engagement processes

- Monitor national implementation timelines and prepare for compliance by 2028

- Align CSDDD efforts with CSRD/ESRS reporting and broader ESG risk management

While CSDDD now targets a narrower group of large multinational companies, companies outside the scope may still face indirect pressure through supply chain expectations or investor scrutiny. Aligning with CSDDD principles can help your company strengthen resilience, reputation and stakeholder trust.

The EU Deforestation Regulation (EUDR)

The EUDR requires that products sold or exported to the EU, including timber, cattle, cocoa, coffee, palm oil, rubber, soy, and their derivatives, are deforestation-free, comply with local laws, and have a due diligence statement.

Both EU and non-EU operators and downstream traders must follow these rules. Large companies must comply by December 30, 2026; smaller firms have until June 30, 2027.

Practical steps for your company to prepare for compliance:

- Check if covered products enter your supply chain or are exported from the EU. Determine your role—operator or trader—as obligations differ. Map your supply chain accurately, including geolocation data.

- Communicate the new requirements to your suppliers and request plot-level geolocation data for commodity sources to verify that production didn’t contribute to deforestation.

- Build traceability systems linking geolocation, supplier details and product batches. These systems will support due-diligence reports, risk assessments and potential audits.

- Assess deforestation risk using country status, satellite data, and supplier info.

- Set up processes for required due diligence statements.

- Treat EUDR compliance as part of an integrated strategy. Align due-diligence systems and data collection with CSRD, CSDDD and broader sustainable sourcing initiatives to meet multiple regulatory and investor expectations simultaneously.

The European Union Emissions Trading System (EU ETS)

The EU ETS is a cap-and-trade system that was established in 2005 to reduce emissions from industry and power generation. In 2023, the EU ETS was revised to include a tighter emissions cap (the emissions cap will be 62% lower by 2030 compared to 2005 levels) as well as new measures to address carbon leakage. Companies that operate in Europe may be subject to emissions allowances or other requirements under this system. Another revision of the EU ETS is planned to be presented in summer 2026, which is expected to have substantial impacts; however, the specific changes and their consequences are not yet clear.

What companies need to know:

- If a company has operations in the EU and is covered under the EU ETS, then it will need to acquire and surrender allowances to cover emissions.

- Industrial sectors covered include:

- Energy-intensive industry sectors, including oil refineries, steel works, and production of iron, aluminum, metals, cement, lime, glass, ceramics, pulp, paper, cardboard, acids and bulk organic chemicals (Free allowances for energy-intensive industries will be phased out from 2026 to 2034);

- Aviation within the European Economic Area and departing flights to Switzerland and the United Kingdom (free allocation of allowances will be removed as of 2026);

- Maritime transport (new in 2024): 50% of emissions from voyages starting or ending outside of the EU and 100% of emissions from voyages between two EU ports and when ships are within EU ports.

- A new emissions trading systems, called ETS2, has been created to cover emissions from buildings, road transport and additional sectors. The new system will become operational in 2027 and complement other European Green Deal policies in these sectors

- Waste incineration: monitoring and reporting of emissions from municipal waste incineration is required in 2024

- Companies not operating in the EU may be indirectly impacted by EU ETS and may have to purchase emission allowances if importing goods into the EU to cover production emissions.

Investing in emission reduction measures and measuring and disclosing your company’s carbon footprint can help you comply with carbon pricing and regulatory requirements like EU ETS. Consulting with policymakers will also help you to understand this changing framework.

Carbon Border Adjustment Mechanisms (CBAM)

The EU’s new CBAM imposes a carbon price on imported goods based on their carbon footprint. Starting January 2026, CBAM enters its implementation phase. In this phase, importers need to declare annually the carbon emissions embedded in their imported goods and purchase CBAM certificates at a price pegged to the EU ETS. As a result of the 2025 omnibus package, no CBAM certificates need to be purchased or surrendered until 2027 and the annual deadline for CBAM declarations was moved from July to September of the following year. As of now, CBAM covers six product categories: iron & steel, aluminum, cement, fertilizers (there is now an exemption for 2026), electricity and hydrogen. It’s expected to expand to more products over time. The UK, Canada, and the U.S. have discussed similar mechanisms to protect their industries and price carbon on imports. Companies should anticipate that carbon border fees could become a global trend in the coming years.

Practical steps for your company to manage CBAM impact:

- Determine if your company exports any CBAM-covered goods to the EU. Also consider if you import these materials into the EU as inputs. Map your trade flows and see where CBAM might apply

- Set up emissions tracking for products. During the transitional phase, importers must report product emissions. This usually means calculating the direct and electricity-related emissions per ton of product at the factory level. Work with your operations teams and suppliers to gather this data. You may need to perform product Life Cycle Assessments or use default values provided by the EU if exact data isn’t available. Invest in accurate carbon accounting at the product level, as this will determine the fees you pay

- If your home country or production facilities already face a carbon price (e.g., participation in an emissions trading system or a carbon tax), ensure you have documentation of those costs. The CBAM rules allow you to reduce your owed certificates by the amount of carbon price already paid abroad.

- For exporters, consider how CBAM might affect the landed cost of your goods in Europe. If your product has a lower carbon intensity than competitors’, highlight that advantage. For importers in the EU, factor in CBAM costs when sourcing materials. In any case, supply chain managers should integrate carbon intensity as a factor in procurement decisions, alongside price and quality.

Green Deal Industrial Plan: Net Zero Industry Act and the Critical Raw Materials Act

The EU has adopted a number of pieces of legislation as part of a “Green Deal Industrial Plan” to decarbonize and revitalize European Industry. Two of the most important are: the Net Zero Industry Act (NZIA) and the Critical Raw Materials (CRM) Act. With these pieces, the Commission aims to establish a regulatory environment that will boost European industry in areas considered crucial for the EU to reach net-zero by 2050.

The NZIA is meant to spur domestic EU production of clean technologies. Main provisions include:

- At least 40% of the annual deployment needs for strategic net-zero technologies manufactured in the EU by 2030.

- Supporting 8 strategic net zero technologies: i) solar photovoltaic and solar thermal technologies; ii) onshore wind and offshore renewable energy; iii) batteries and storage; iv) heat pumps and geothermal energy; v) electrolyzers and fuel cells; vi) biogas/biomethane; vii) carbon capture and storage (CCS); and viii) grid technologies.

- Proposals for Net-Zero Strategic Projects, Accelerating CO2 capture and storage, facilitating access to markets, Net-Zero Industry Academies, accelerated permitting, Net-Zero Europe Platform and the European Hydrogen Bank.

The CRM Act aims at securing the EU’s supply of CRMs necessary to power the transition. Main provisions include:

- Extract more in Europe – 10% by 2030.

- Refine – 40% in EU by 2030.

- 15% of the Union’s annual consumption of strategic raw materials comes from recycling.

- Provision on joint purchasing of raw materials.

Further important industrial rules and support are expected in the Industrial Accelerator Act in 2026.

Extended Producer Responsibility (EPR)

In February 2025, the EU formally adopted the Packaging and Packaging Waste Regulation (PPWR) imposing stronger obligations on producers of packaging in order to reduce waste. Key provisions include mandatory recyclability of all packaging by 2030, recyclability performance grades for packaging from 2025 onward, minimum recycled content targets for plastic packaging and multiple measures to curb excess packaging and promote reuse. Extended Producer Responsibility (EPR) is central to PPWR. It requires producers to cover the full costs of collecting, sorting and recycling packaging waste and to encourage eco-design.

Companies that manufacture, import, or sell products in the EU may be subject to EPR obligations, especially in the following sectors:

- Packaging

- Electrical and electronic equipment

- Batteries and accumulators

- Textiles (new EU-wide EPR for textiles enters into force in 2025. Member States now have until April 2028 to establish operational textile/footwear EPR programs)

- Vehicles, furniture, and other durable goods (in some Member States)

Even if your company is not directly subject to EPR, you may be impacted as a supplier to EU-based producers who are required to report on and manage their product-related waste.

The key requirements are:

- Registration with national Producer Responsibility Organizations (PROs) in each Member State where products are sold

- Reporting of product volumes placed on the market, material composition, and recyclability

- Payment of eco-modulated fees based on product sustainability. This means companies will pay higher fees for packaging materials that are hard to recycle, and lower fees for packaging that is easily recyclable, reusable, or made from recycled content

- Participation in take-back schemes or funding of waste collection and recycling infrastructure

Case Study

Berlin’s Reuse Pilot

For years, reusable packaging was seen as a niche sustainability initiative. The Berlin pilot shows that it can be a practical business strategy that reduces costs, meets regulatory expectations and improves customer engagement. Learn more about it here

Practical steps for your company to prepare for compliance:

- Assess whether your products fall under EPR categories in the EU or specific Member States

- Map your obligations across jurisdictions where your products are sold or distributed

- Engage with local PROs to understand registration, reporting, and fee requirements

- Review product design and packaging to reduce EPR fees through improved recyclability or use of recycled materials

- Coordinate with sustainability and compliance teams to align EPR data with CSRD/ESRS reporting and circularity goals

- EPR is rapidly evolving and expanding across the EU. Companies should monitor developments at both the EU and Member State levels and integrate EPR compliance into broader sustainability and product stewardship strategies.